Shutterstock

By Brian Lucey and Shaen Corbet| August 17, 2018

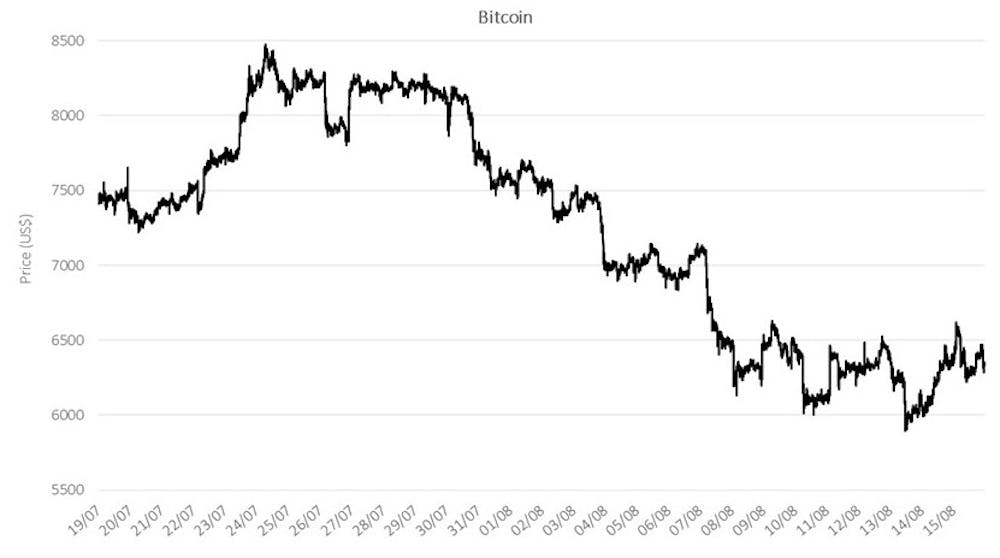

The rollercoaster of cryptocurrency pricing is on the downward slope again. Bitcoin has fallen by a quarter in the past month, with other large currencies such as Ethereum and Ripple down more than 40%. So where does this latest bout of losses leave cryptocurrencies?

Sceptics point to the multitude of regulatory issues and avenues for fraud and outright theft. Advocates continue to insist that these are the “future of finance”.

Bitcoin’s slide over the last month.

One of the reasons for the latest sell-off is that investors are selling their crypto to pay off the capital gains tax they are required to pay on their gains. It has been estimated that US$25 billion is owed in the US alone.

But there is a more fundamental issue at play of investors rushing to convert their profits from initial coin offerings (or ICOs) into fiat currency like dollars. This is where a new crypto token is created in exchange for existing cryptocurrencies like bitcoin.

The lack of regulation to protect the profits made from ICOs reflects the wider issue facing the future of crypto. If cryptocurrencies are to become a more mainstream asset, they will require regulation – but this will be unpopular with much of its existing fan base which is inherently libertarian.

ICO trouble

The transfer of crypto gains from an ICO to fiat currency can generate quite the scrummage as cryptocurrency investors attempt to exit the market with the largest amount of value possible. In early 2018, it was reported that almost 46% of 2017 ICOs had already failed.

The pressure to exit in a timely manner has been exacerbated by the substantial number of ICO scams that have taken place. Crypto analysis site Diar estimates that, since 2017, nearly US$100m had been lost to ICO exit scams where organisers have little or no intention of developing a financial product that will perform to the standard that is advertised to investors.

The cryptocurrency world is largely unregulated and so ripe territory for scammers to operate. Fraud in cryptocurrency markets has to date taken multiple forms. As well as ICO issues, there has been fraud at exchange level, the most famous example of which was the collapse of the Mt. Gox exchange which once handled 80% of global bitcoin trading.

The number of issues and vast sums of money involved has resulted in the US Securities and Exchange Commission casting its supervisory gaze on the crypto world.

Substantial questions

A growing body of academic research has raised substantial questions over the true underlying integrity of cryptocurrency markets. It highlights the various areas where regulation is needed if bitcoin and others are to have a viable future.

For example, economist Neil Gandal and colleagues found that trading volumes on all Bitcoin exchanges increased substantially on days where they found suspicious trading activity. The authors demonstrated that this suspicious activity by one single actor or agent was most likely a big factor behind the sharp increase in the price of Bitcoin from US$150 to US$1,000 in late 2013.

Declines in liquidity have also been found to contribute to the risk of a crash in Bitcoin. This is problematic given that, even under normal trading conditions, Bitcoin is found to be more volatile, less liquid and costlier to transact than other assets.

Finance researchers John Griffin and Amin Shams analysed blockchain data and found that tether, a cryptocurrency pegged to the US dollar, deeply influenced other cryptocurrencies during the sharp price appreciations of 2017 and 2018. They concluded that tether transactions were responsible for up to 50% of the increase of Bitcoin and 64% of the increase in value of other top cryptocurrencies.

Our own research has suggested that cryptocurrencies are only very lightly linked to other financial or economic assets, and that the majority are unaffected by the main market announcements. This all goes to show that cryptocurrencies can be manipulated and do not reflect normal market activity.

The underlying economic value of cryptos has also been evaluated, with some suggesting that a crypto’s value is determined solely by the willingness of its holders to hoard. Others have found that crypto values are mainly a function of their network depth and not their intrinsic usefulness – again leaving it open to manipulation. Still others point to the economic limits to bitcoin arising from its mining cost.

Strangely, we now live in a world where joke cryptocurrencies such as the Useless Ethereum Token and Fuzzballs have tangible value, despite being miniscule in comparison to Bitcoin or Ethereum. The former advertises itself with the statement: “Seriously, don’t buy these tokens”, the latter contains a warning on its website stating: “There seems to be a problem with the Fuzzballs chain/source” and “mine Fuzzballs at your own risk.”

Would a neutral, independent observer look at these facts and buy these tokens? What would an observer that survived the dot-com crash think?

To be merited as a somewhat viable and trustworthy financial market product, cryptocurrencies must in some way adhere to a common standard of international regulation. Until this occurs, we will continue to observe situations involving substantial theft from international exchanges, continued disquiet as fraudulent ICOs are uncovered with investor funds channelled around the world, and most interestingly, a market that has become so sensitive to minute details that even the smallest hint of strife can generate substantial price volatility.

![]()

The challenge for proponents of cryptocurrencies is how to continue to promote their decentralised, anonymous, libertarian nature as their issuance and trading become more and more regulated.

Brian Lucey, Professor of International Finance and Commodities, Trinity College Dublin and Shaen Corbet, Assistant Professor (Finance), Dublin City University

This article was originally published on The Conversation. Read the original article.